Account Updater Flow

Each card brand has their own version of account updater, and each version requires its own unique integration. Once integrated, you’ll receive updated card information via the following flow for each individual card brand:- You submit a request to the card brand for updated card details.

- The card brand sends an update request to the issuing bank.

- The issuing bank processes the update request and returns updated card details to the card brand.

- The card brand returns the card details to you.

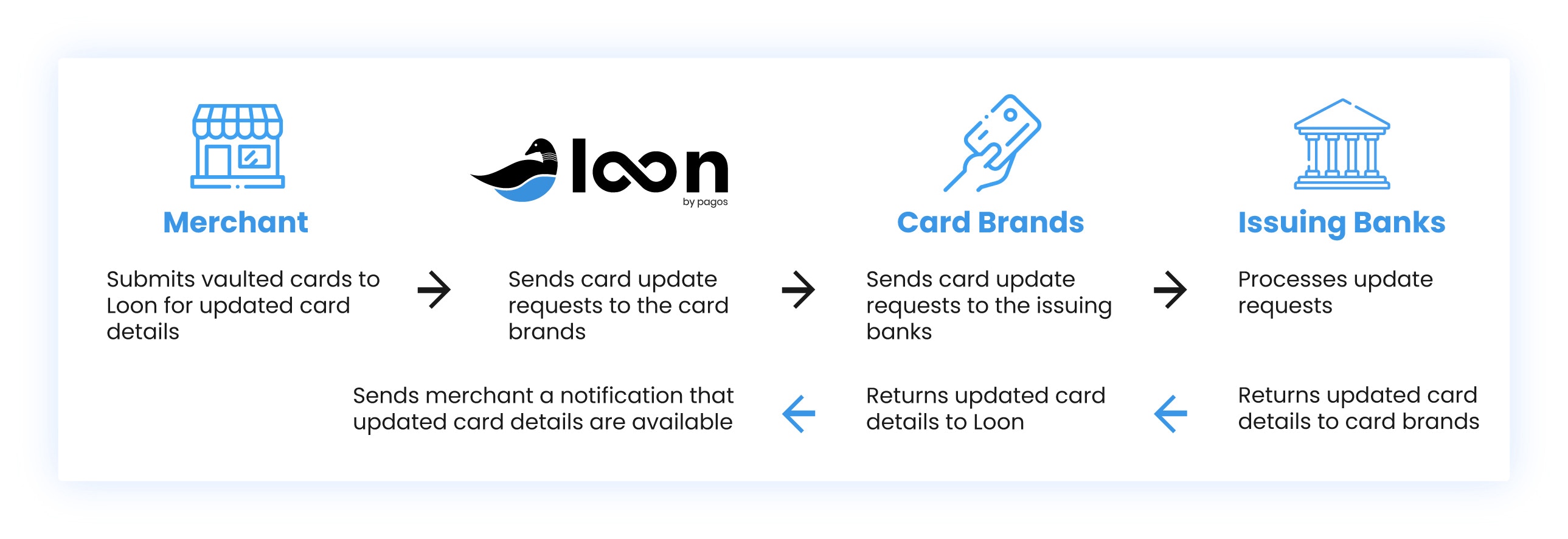

Account Updater Flow With Pagos

Pagos’ Account Updater is an easy-to-use, global solution that is independent of card brands or payment service providers. With Pagos, you only need to manage one relationship, one integration, and you’ll get access to account updater services and data for all four major card brands (Visa, Mastercard, Amex, and Discover)—regardless of your processor or processors. The flow with Pagos looks like this:

Benefits of Account Updater

Inevitably, vaulted card details will change and go stale. Account updater programs ensure you stay on top of changes, thus improving approval rates, reducing churn, and providing better customer experiences with your brand.Increasing Approval Rates

Using an account updater solution can decrease how often issuing banks decline your authorization attempts because of outdated cardholder payment information. Examples of these types of declines include:- Card has expired or the expiration date has changed

- Card has been updated due to being lost or stolen

- Card has been reissued due to a new card program, a new card brand, or fraud

- Customer details such as customer name or address have changed