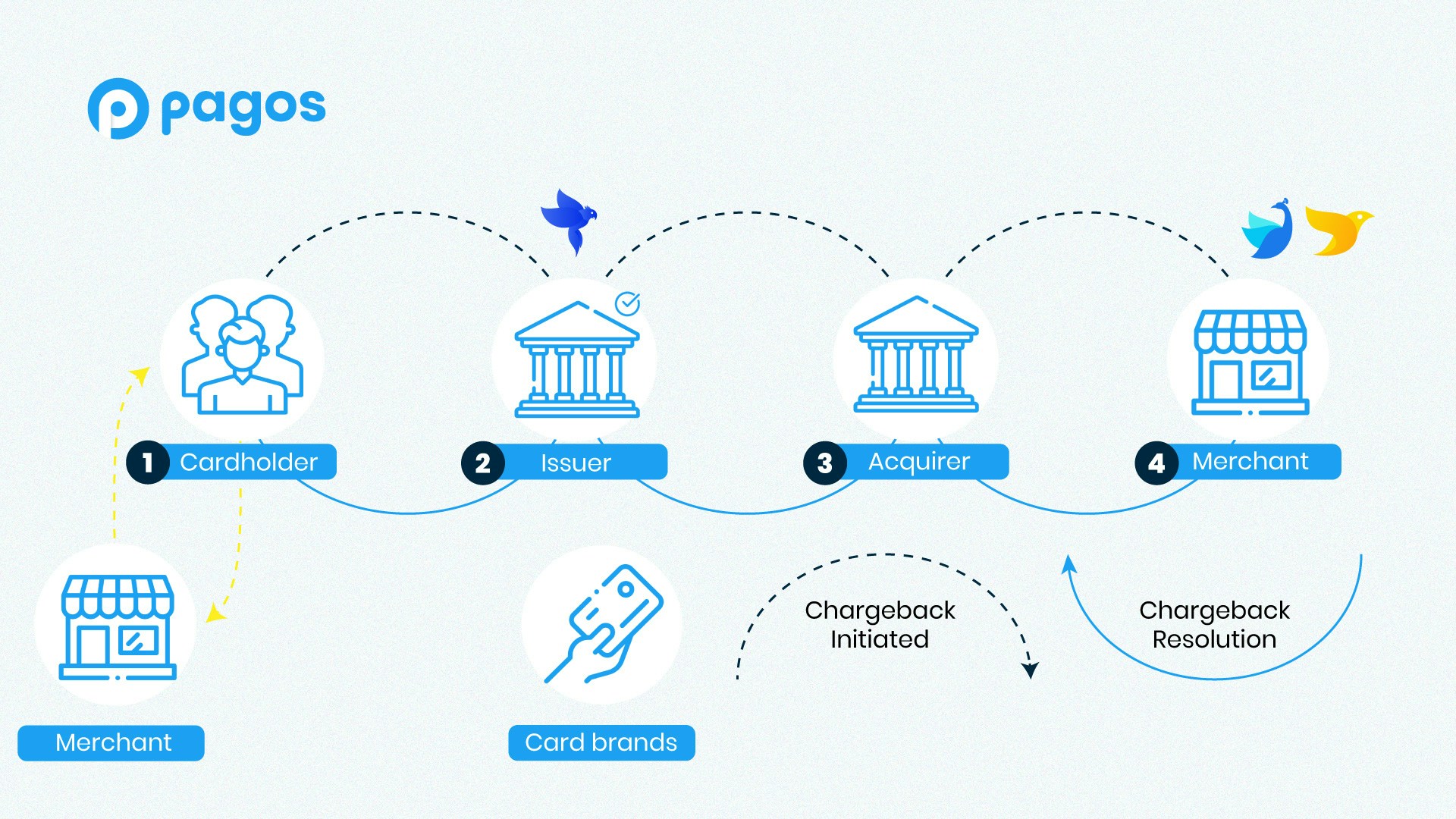

Step 1: Initiating the Chargeback

Chargebacks typically start when a cardholder questions the validity of a charge and files an official dispute with their issuing bank. Cardholders can issue disputes for any number of reasons, such as not recognizing the charge on their bill, not receiving a refund or credit that was initiated or promised by the merchant, dissatisfaction with the product or service rendered, delivery issues, or suspected fraud.Issuing banks can also initiate chargebacks when they identify authorization or processing errors, or suspect merchant fraud. These types of disputes are known as bank chargebacks.

Reason Codes

Chargeback reason codes fall into four general categories:- Authorizations – These include processing a transaction without obtaining an authorization, processing on a declined authorization, or failing to include an authorization in the settlement file for a transaction

- Processing errors – These are mostly bank chargebacks, and often result from late presentment, processing the incorrect currency, or duplicate processing

- Fraud – These can indicate either true fraud or friendly fraud

- Consumer-initiated disputes – These are largely related to service issues, such as the customer not receiving the merchandise or services, canceled recurring payments, merchants failing to properly process a customer’s return, or items not appearing as described or defective

Step 2: Passing the Chargeback to the Merchant

After receiving a chargeback from the issuing bank, the acquiring bank may auto-reply on the merchant’s behalf. Otherwise, they’ll forward the chargeback along to the affected merchant and immediately debit the amount of the chargeback—plus any associated fees—from the merchant’s daily settlement report.If the merchant’s total sales for the day are less than the sum of all refunds, credits, and chargebacks, this can result in a rejection of some initiated refunds (which can lead to even more chargebacks). As such, it’s critical that merchants monitor their net daily and settlement transaction values.

Step 3: Presenting Evidence Against the Chargeback

If the merchant decides to defend themselves against the chargeback, they must provide compelling evidence in accordance with card brand rules to contradict the chargeback claim and prove the transaction’s validity. Such proof can include:- The merchant’s public Terms of Service

- Proof of accurate terms of sale communicated to the customer prior to the transaction

- A substitute record of charge that clearly states the date of sale

- Proof of shipping records or product delivery

- Copies of customer service communications where the transaction was discussed and agreed to by the customer, or where the customer attempted to cancel the transaction when such an action was not within the merchant’s policies

- The status of any returns