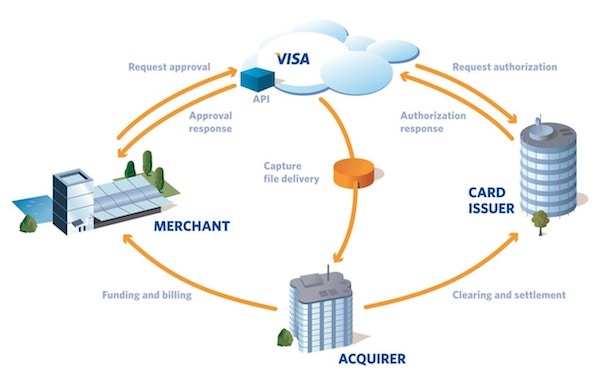

The Role of Card Brands

First let’s lay out the key parties in payment processing, and where card brands come into play.

- Merchants - Businesses that accept card transactions from their customers in exchange for goods and services

- Acquirers - A bundle of services including a bank, processing company, and gateway that provide merchant accounts to merchants, allowing them to collect funds from issuers’ cards for successful transactions

- Card issuers - A bank and a processing company who provide payment cards (credit, debit, and pre-paid) to consumers

- Card brands (Visa in this case)

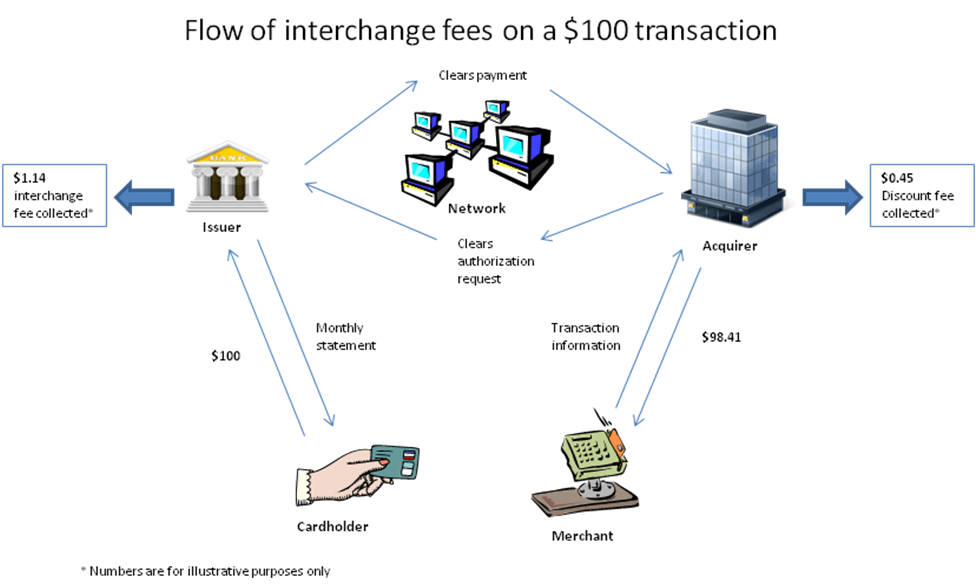

Interchange

In short, interchange is the money acquiring banks pay to issuing banks to compensate them for providing cardholders with credit lines and servicing which, in turn, allows merchants to make bigger and more frequent sales. When setting interchange rates, the network critically takes into account the value of the transaction to merchants, the operational cost of moving money, and the risk associated with providing credit to both merchants and consumers. In practice, interchange becomes a big part of the merchant discount rate (MDR) that a merchant pays to their acquirer for providing both access to the network and the technical and processing services required for processing payments (e.g. terminals in the traditional retail scenario and gateways online). It should be noted that interchange doesn’t include other passthrough costs like the card brand’s assessment fees and other processing fees that your gateway, processor, or acquiring bank charge.Side Note:

When we talk about the risk associated with cards, it is worth noting some key differences based on the type of card:

- For credit cards, card network rules require issuing banks to pay merchant acquiring banks before the cardholders have paid their monthly bill. As such, businesses get paid right away for their card transactions (or within 2 days depending on the setup), and the issuing bank has to collect that money from their card customers several days or even months later, thus generating more risk.

- With debit cards, however, the risks are usually much lower, because the money for a transaction often comes from available funds in a bank account.

- Credit vs. debit card

- Traditional vs. premium card

- Local (i.e. within the same country as the merchant/company) vs. cross-border

- Security flags and features: CVV, AVS, 3DSecure, etc.

- Regulation: increasingly governments around the world are regulating payment costs

Interchange Downgrades

Card brands set interchange rates for different categories of transactions based on an established set of requirements. If a transaction doesn’t meet all of the requirements, it will be downgraded to a different category with a higher interchange rate. For example, a transaction might qualify for a lower “CPS/Retail” rate if processed with AVS and CVV data, but get downgraded to a higher “Standard” rate if that data is missing. To prevent downgrades, you need to follow the associated requirements for the types of cards you accept and the processing environments you use (in-person vs. online, CIT vs MIT, etc.)Further Reading:

- Glenbrook Payment Systems in the US — great introduction to how various payment systems work in the US.

- Credit/Debit Card Interchange Fees – Assessed to Merchants in U.S. – an example report from the Fed Reserve Bank of Kansas City (August 2020)

- U.S. Interchange: Visa / Mastercard

- E.U. Interchange: Visa / Mastercard