Mastercard Enhanced Data

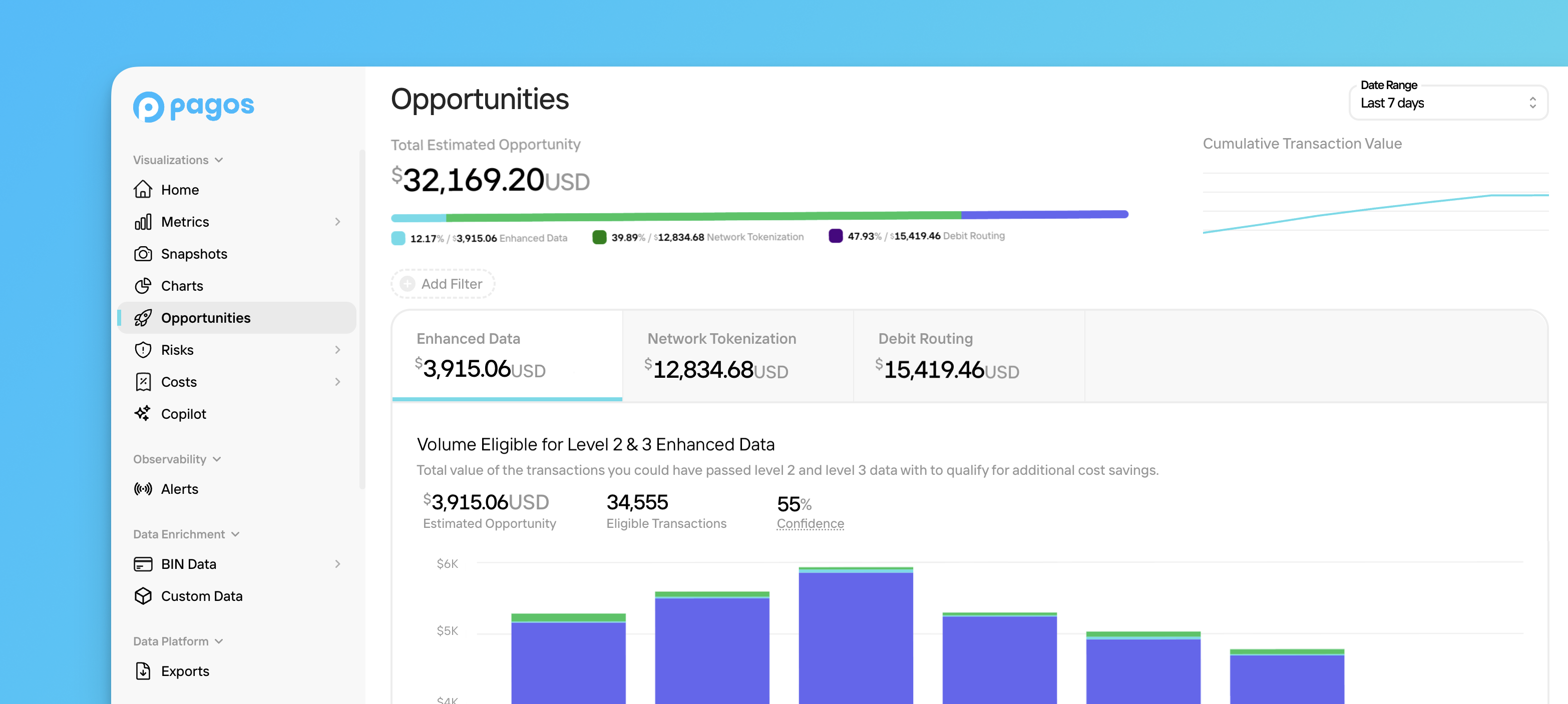

Some Mastercard payment cards qualify for Level 2 or Level 3 processing, meaning if you collect and pass specific information (e.g. sales tax amount, order number, product description, etc.) when processing transactions with those cards, you’ll face lower interchange rates. In the Mastercard Enhanced Data tab, you’ll find the following data:- Estimated Opportunity - The total amount you could have saved, had you passed Level 2 & 3 data with your Mastercard transactions; the graph below demonstrates these estimated savings over time, broken down by their qualification for only Level 2, Level 2 or 3, and only Level 3 savings.

- Eligible Transactions - The number of Mastercard transactions you processed that were eligible for Level 2 & 3 data.

- Confidence - Pagos estimates your savings with 55% confidence. This confidence level reflects a key data limitation: we can’t identify how much of your eligible transaction volume actually included enhanced data. Instead, we estimate your savings based on historical data showing the average merchant omits enhanced data on 60–75% of eligible transactions.

Network Tokenization

Network tokenization is the process through which card brands substitute a cardholder’s primary account number (PAN) and other card details with a secure, unique value known as a network token. There are many benefits to network tokenization, including increased data security, increased approval rates, and improved customer experiences. Some transactions also qualify for lower interchange rates when processed with a network token instead of a PAN; the estimated opportunity in this tab represents the transactions for which these savings exist. In the Network Tokenization tab, you’ll find the following data:- Estimated Opportunity - The total amount you could have saved in interchange costs had you processed eligible transactions with network tokens instead of PANs; the graph below demonstrates these estimated savings over time.

- Eligible Transactions - The number of approved, card transactions you processed with PANs that could have been processed with network tokens instead.

- Confidence - Pagos estimates your savings with 90% confidence using average savings values across historical cost data.

Australia

Australia

- Card Brands - Visa and Mastercard

- Card Types - Credit, debit, and prepaid

- Issuing Country - Australia

- Stored Credential - Recurring, card-on-file, or installment

United States

United States

- Card Brand - Visa

- Card Types - Credit

- Card Product Category - Consumer

- Issuing Country - United States

- Stored Credential - Recurring, card-on-file, or installment

See DCAP and Visa Network Token Savings section below for more information on US savings opportunities.

Japan

Japan

- Card Brand - Visa

- Card Types - Credit and debit

- Card Product Category - Consumer and business

- Issuing Country - Japan

- Stored Credential - Recurring, card-on-file, and installment

DCAP and Visa Network Token Savings

When Visa launched the Digital Commerce Authentication Program (DCAP) in April 2026, they reduced the available network token interchange savings from 10bps to 5bps for Visa consumer credit cards processed in the United States. The US data in the Network Tokenization Opportunities tab reflects this reduction. We don’t display the potential savings available on transactions that are both tokenized and DCAP-qualifying. As such, your interchange savings could increase if you pass qualifying customer and device data and receive DCAP savings on top of network token savings.Debit Routing

As of July 2023, issuing banks in the United States must ensure all card-not-present debit transactions can be processed by at least two non-affiliated networks. This change created more competition among debit networks, leading to them offering reduced interchange rates by up to 30% to merchants who route debit transactions through their networks. In the Debit Routing tab, you’ll find the following data:- Estimated Opportunity - The total amount you could have saved had you processed eligible US debit transactions through an alternative debit network; the graph below demonstrates these estimated savings over time, broken down by whether they’re associated with cards issued by Durbin-regulated vs unregulated banks.

- Eligible Transactions - The number of US debit transactions you could have processed through an alternative debit network.

- Confidence - Pagos estimates your savings with 65% confidence. This confidence level reflects the following data limitation: we can’t identify exactly how much of that eligible transaction volume you did route to lower cost networks. Instead, we estimate your savings based on historical data showing the average merchant routes half of their eligible volume to alternative debit networks.

Visa CEDP Calculator

Visa incentivizes businesses to collect and pass quality enhanced data with transactions through their Commercial Enhanced Data Program (CEDP). Stricter than their prior L2/L3 programs, CEDP introduces a verification-driven approach, whereby merchants can only receive lower interchange rates on commercial transactions once Visa verifies their compliance with new enhanced data requirements. Visa charges a 0.05% CEDP participation fee on every enhanced-data transaction, regardless of whether the transaction qualifies for an interchange reduction. In the Visa CEDP Calculator tab, use the following sliders to estimate your CEDP savings or costs:- Participation Rate - Estimate the percentage of your total eligible transactions for which you’re currently submitting enhanced data.

- Data Quality Rate - Estimate what percentage of enhanced-data transactions you submit that actually meet Visa’s quality standards and would receive the interchange reduction.